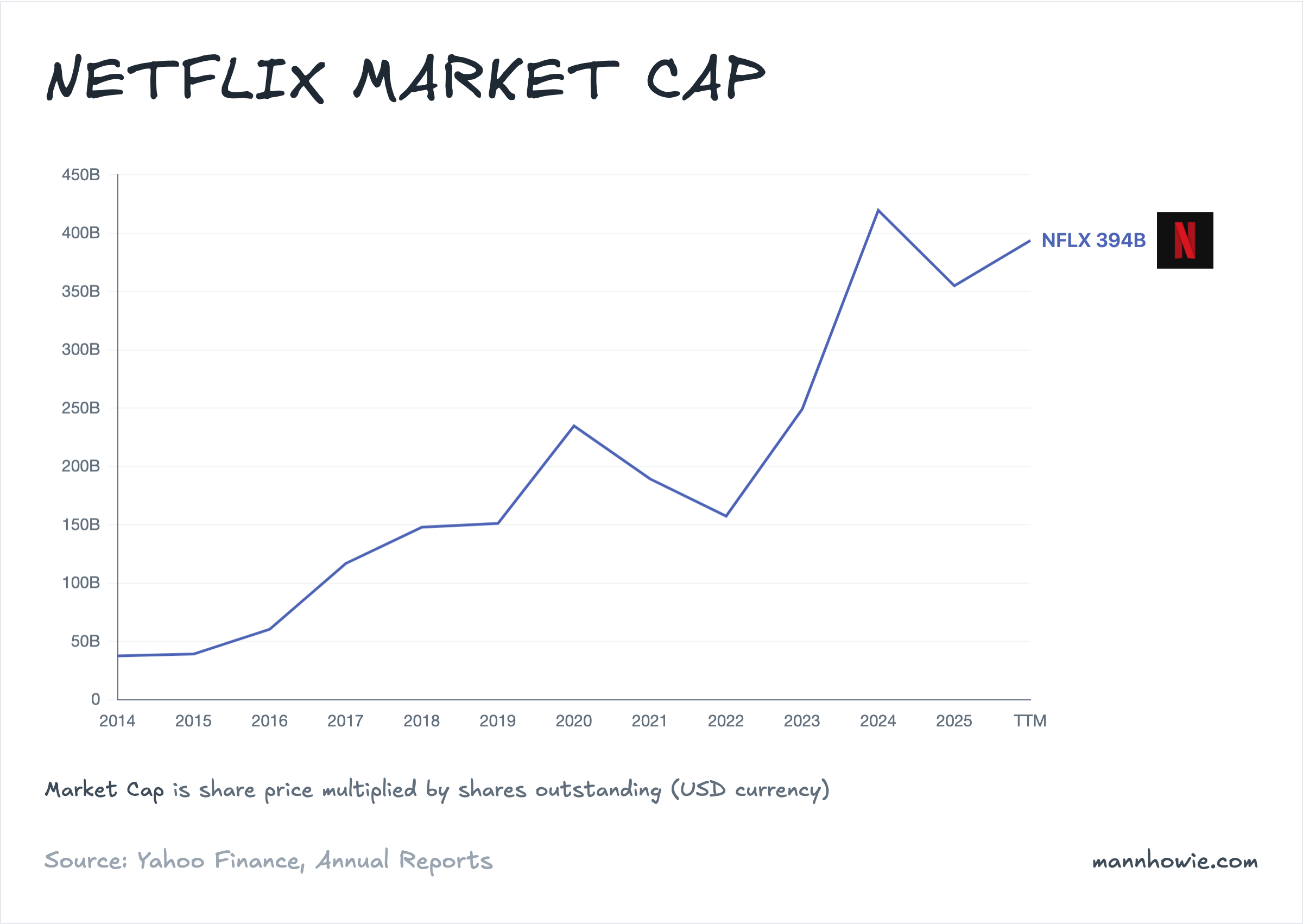

Netflix: the price lever, the lost bid, and the defense

7 minute read | Apr 23, 2026 | Reviewed by Howie Mann

Netflix streams films, series, games and a small but growing slate of live events to subscribers in over 190 countries. The business runs on monthly subscription fees and, since late 2022, advertising on a lower-priced tier.

Advertising grew two-and-a-half times in 2025 to about $1.5B. Guidance is to double again to $3B in 2026. Netflix stopped disclosing paid memberships in FY2025. The metric that now matters is dollars per subscriber.

Netflix raised prices, held content flat, and doubled its margin

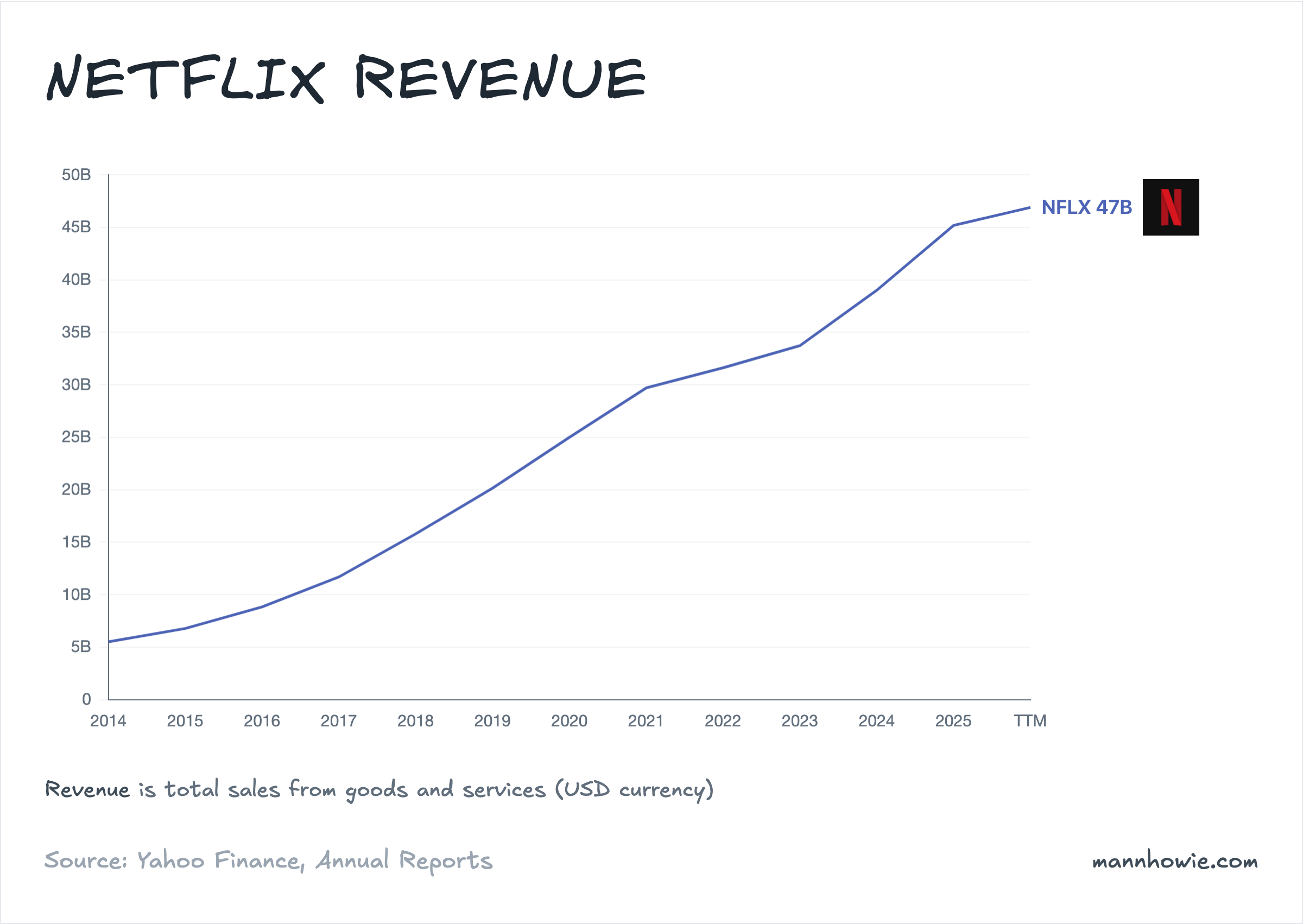

Revenue grew $13.6B in three years. Subscribers grew too, from 230.7M at the end of FY2022 to more than 325M at the end of FY2025. But Netflix stopped reporting the number. Management shifted its primary metrics to revenue and operating margin. Subscribers were no longer the story. Dollars per subscriber were.

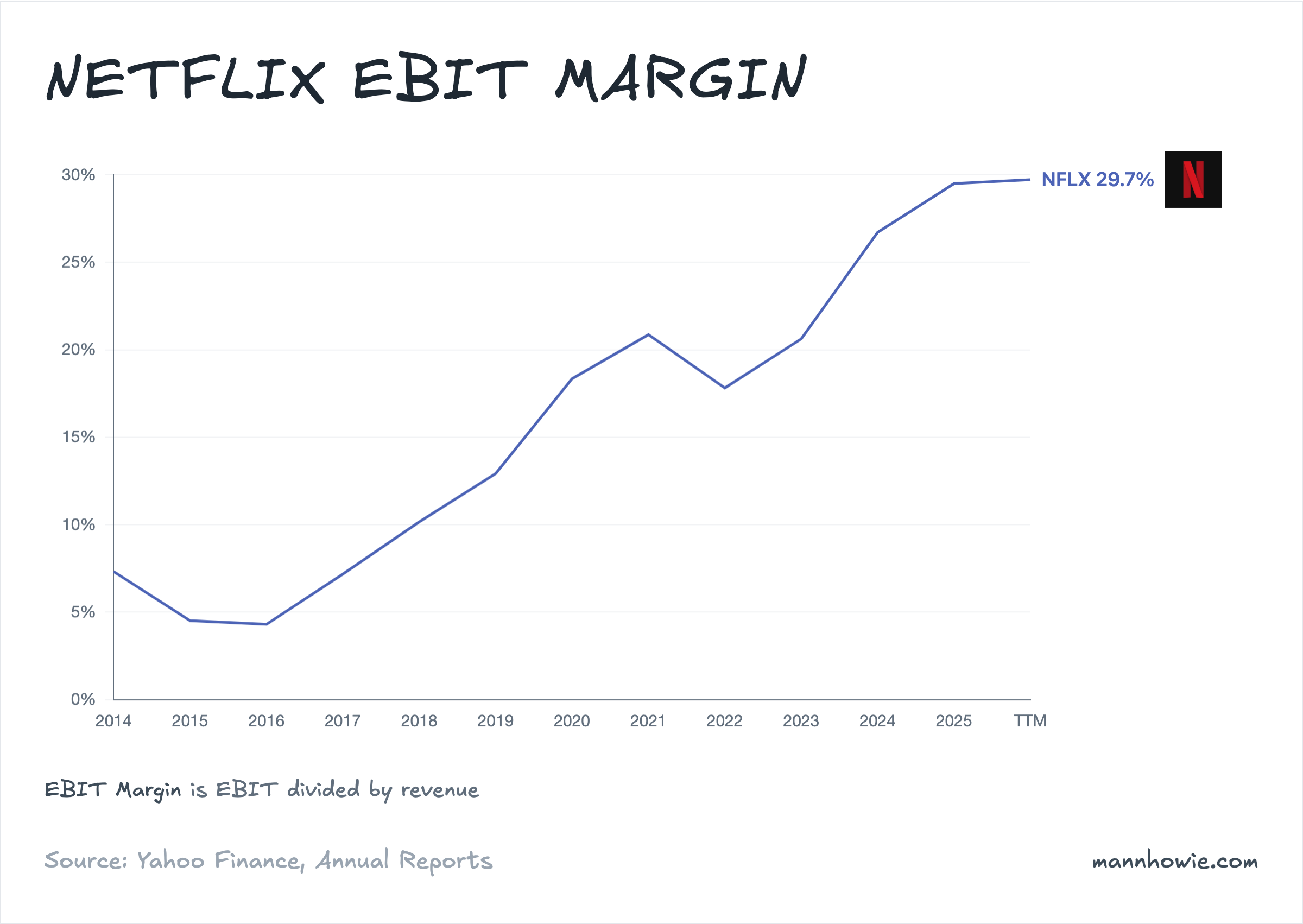

Operating margin went from 17.8% in FY2022 to 29.5% in FY2025, with 2026 guided at 31.5%. Twelve margin points in three years. The mechanism is two levers pulled at once: average revenue per membership was raised hard in the US while content cash spend was held flat at about $17B. Revenue climbed 43% over the window. Content spend did not.

| Region (ARM, USD/month) | FY2019 | FY2022 | FY2024 | 5Y Change |

|---|---|---|---|---|

| United States and Canada | 12.57 | 15.86 | 17.20 | +37% |

| Europe, Middle East, Africa | 10.33 | 10.99 | 10.96 | +6% |

| Latin America | 8.21 | 8.48 | 8.24 | +0% |

| Asia-Pacific | 9.24 | 8.50 | 7.29 | −21% |

| Global blended | 10.82 | 11.76 | 11.70 | +8% |

US and Canadian subscribers are paying 37% more than they were five years ago. Asia-Pacific is paying 21% less, as Netflix chased subscriber growth in India at lower price points. The margin engine runs on North American households. Netflix stopped ARM disclosure in FY2025, so the table ends at FY2024.

The competitive field just moved

The playbook above assumed a weak field. Disney’s Direct-to-Consumer segment lost $2.5B in FY2023. Warner Bros. Discovery was absorbing the Discovery merger under $40B of debt. Paramount was in restructuring. All three of those assumptions broke in 2025.

“YouTube is not just UGC and cat videos anymore. YouTube has full-length films. New episodes of scripted and unscripted TV shows. They have NFL football games. They have the Oscars. The BBC is going to be producing original content for YouTube soon. They are TV. So we all compete with them in every dimension.”

— Ted Sarandos, Netflix Q4 FY2025 earnings call

YouTube generated more than $60B across advertising and subscriptions in 2025, according to Alphabet. Netflix’s entire business generates $45B. Nielsen has ranked YouTube the number-one streamer in the US by TV-time for three consecutive years. A category Netflix has never led.

Netflix tried to consolidate and lost. In December 2025 Netflix signed to buy Warner Bros. Discovery for $82.7B including debt. The deal would have brought in the studio, HBO, CNN and a century of Warner library. Paramount Skydance topped the bid in February 2026 at $110.9B. Warner’s board accepted the superior proposal. Netflix walked with a $2.8B termination fee. The library Netflix was going to buy is now moving inside a rival backed by fresh capital.

Disney and Prime are no longer on the sidelines. Disney DTC swung from that $2.5B loss to $1.3B of operating profit in FY2025 on $24.6B of revenue. It carries a library Netflix cannot match at any price: Marvel, Pixar, Lucasfilm, Walt Disney Animation. Prime Video sits inside a $139 Prime membership. Amazon bundled Prime Video ads in 2024 without dropping the subscription price and does not need the service to stand on its own.

Where growth goes from here

Netflix’s answer is not a new content library. It is three levers already in motion, made more explicit in the Q1 2026 earnings call after the Paramount outbid.

International is lifting. The regions that grew fastest in dollar terms over the last three years are not the US.

| Region (USD M) | FY2022 | FY2025 | 3Y CAGR | 3Y Change ($) |

|---|---|---|---|---|

| United States and Canada | 14,085 | 19,957 | 12.3% | +5,872 |

| Europe, Middle East, Africa | 9,745 | 14,515 | 14.2% | +4,770 |

| Asia-Pacific | 3,570 | 5,354 | 14.5% | +1,784 |

| Latin America | 4,070 | 5,358 | 9.6% | +1,288 |

| Total | 31,470 | 45,183 | 12.8% | +13,713 |

EMEA and APAC both compounded faster than the US on smaller bases. In Q1 2026, management said Asia-Pacific was Netflix’s strongest FX-neutral revenue growth market. Japan posted its highest quarter of paid net adds on record, driven by the World Baseball Classic: 31.4 million viewers, the largest global baseball stream on any platform. India, Korea and Southeast Asia each ran ahead of the US.

Original content over Hollywood library. Management reframed the WB walk-away as discipline, not defeat. “The WB deal was a nice to have, not a need to have,” Sarandos said in April. “When the cost of this deal grew beyond the net value to our business and to our shareholders, we were willing to put emotion and ego aside and walk away.” The forward slate leans on exclusive original IP: Greta Gerwig’s Narnia, Cillian Murphy’s Peaky Blinders: Immortal Man, a second season of the live-action One Piece, Colombian series A Hundred Years of Solitude. Netflix has also signed licensing deals with Sony (global pay-one films), Universal (live action) and Paramount.

The ad tier as second monetisation lever. Advertising revenue is guided to double to $3B in 2026. Netflix’s advertiser base grew 70% in 2025 to more than 4,000 buyers. Programmatic spend is on track to clear 50% of non-live ad revenue. Ad-tier ARM still sits below the ad-free plan, but the gap is narrowing as Netflix’s in-house ad stack, deployed in 2025, closes the fill-rate and pricing gap.

One defense that is not in the presentation: the US price lever itself. In Q1 2026, management framed further US price increases by noting that Netflix subscribers pay the least per hour of viewing of any major SVOD service in the United States. “In some cases, you’d have to pay 2x per hour to get a competitive service.” The lever that doubled the margin is not, in management’s view, exhausted yet.

Sources

- Netflix 10-K FY2024, pages 19–23 (regional revenue and ARM FY2022–FY2024).

- Netflix 10-K FY2025, pages 20–21, 39, 41 (regional revenue FY2023–FY2025; content assets).

- Netflix Q4 FY2025 earnings call, January 20, 2026 (2026 guidance, ad revenue, YouTube framing, content slate).

- Netflix Q1 FY2026 earnings call, April 16, 2026 (Warner Bros. walkaway commentary, APAC growth, World Baseball Classic, advertiser base, US pricing rationale).

- Sundar Pichai, Alphabet Q4 2025 Earnings Call CEO Remarks, February 4, 2026 (YouTube revenue of $60B+).

- Disney 10-K FY2025, pages 36–47 (Direct-to-Consumer revenue and operating income).

- CNBC, TechCrunch: Paramount Skydance / Warner Bros. Discovery acquisition timeline, December 2025–February 2026.